DREAM.PLAN.ACT.ACHIEVE.REPEAT

Why Most Budgets Don’t Stick

If you’ve ever sat down to make a budget only to abandon it halfway through the month, you’re not alone. According to studies, most people quit budgeting because it feels restrictive, complicated, or unrealistic.

The truth? A monthly budget should feel like freedom, not punishment. Done right, it’s not about limiting your spending—it’s about giving every dollar a job so you can stress less and save more.

Here’s a step-by-step framework for creating a monthly budget that actually works.

Step 1: Calculate Your Monthly Income

Start with your take-home pay—what hits your bank account after taxes. Include:

-

Paychecks

-

Freelance/side hustle income

-

Passive income (dividends, rental, etc.)

This is the foundation of your budget. If your income changes month to month, use a conservative average (aim low to avoid surprises).

Step 2: Track Your Expenses

Before you set limits, know where your money currently goes. Track:

-

Fixed Expenses (rent, utilities, insurance)

-

Variable Expenses (food, gas, shopping)

-

Occasional Expenses (birthdays, holidays, car repairs)

👉 Pro Tip: Review your last 2–3 bank statements to get accurate numbers.

Step 3: Choose a Budgeting Method

Pick a system that matches your personality:

-

50/30/20 Method → Simple, flexible.

-

Zero-Based Budgeting → Great for detail-lovers or debt payoff.

-

Envelope System → Perfect for overspenders who need strict limits.

(See our guide on 5 Beginner-Friendly Budgeting Methods for a deeper dive.)

Step 4: Set Realistic Spending Limits

Based on your method, assign money to categories. Make sure to include:

-

Needs (housing, food, utilities)

-

Wants (dining, shopping, entertainment)

-

Savings/Debt Payoff (emergency fund, investments, loans)

Keep it realistic. If you cut groceries from $600 to $200 overnight, you’ll give up quickly.

Step 5: Build in a Buffer

Life happens—unexpected expenses always show up. Add a small “miscellaneous” category (even $50–100) to protect your budget.

Step 6: Track Weekly, Not Just Monthly

Budgets fail when you only check at the end of the month. Review weekly so you can adjust in real time.

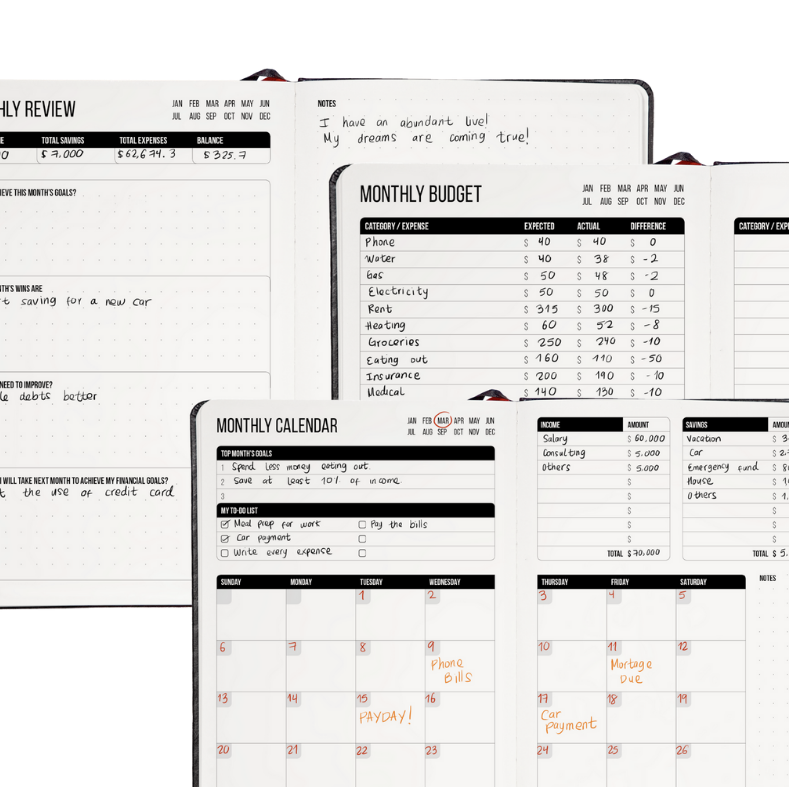

The ThisIsMyEra Budget Planner makes this easy with monthly spreads plus weekly check-ins—so you always know where you stand.

Common Budgeting Mistakes to Avoid

-

Forgetting irregular expenses

-

Being too strict, then “rebelling” mid-month

-

Not writing it down (if it’s only in your head, it won’t last)

-

Skipping weekly reviews

How the Budget Planner Helps

With the ThisIsMyEra Budget Planner, you can:

-

Record income + expenses monthly

-

Set category limits

-

Track savings goals

-

Do weekly check-ins

Free Resource: Monthly Budget Worksheet

We created a free Monthly Budget Worksheet you can download and use right away. Pair it with your Budget Planner for the best results.

Your Money, Your Plan

A monthly budget that actually works is one that fits your lifestyle—not someone else’s. Start with your income, track your spending, pick a method, and check in weekly.

Your future financial freedom is built one month at a time. Get started today with the free worksheet, and let the Budget Planner keep you accountable every step of the way.

FAQs

-

A: Aim for 20% of your income, but even 5–10% consistently adds up.

For all general inquiries, please contact us at info@thisismyera.com

© Copyright. All rights reserved.